In a linear regression model defined as:Y=b0+b1X1

where Y represents salary and X1 represents years of experience, I would like to understand why Euclidean distance (or Euclidean error calculation) is used in the model.

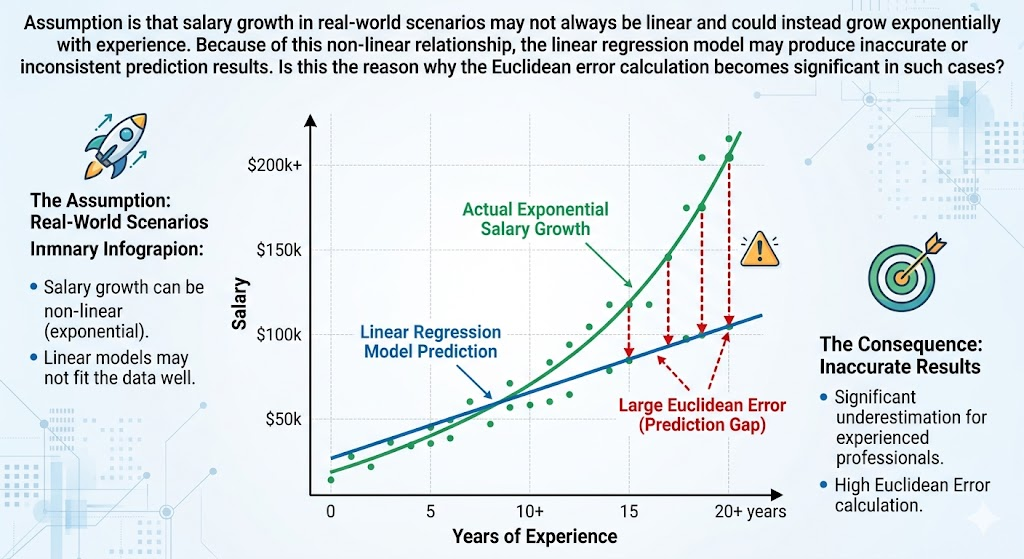

Assumption is that salary growth in real-world scenarios may not always be linear and could instead grow exponentially with experience. Because of this non-linear relationship, the linear regression model may produce inaccurate or inconsistent prediction results. Is this the reason why the Euclidean error calculation becomes significant in such cases?

In a simple linear regression model:Y=b0+b1X1

where:

- Y = Salary

- X1 = Years of Experience

- b0 = intercept

- b1 = slope (salary increase per year)

the Euclidean calculation appears because the model tries to measure how far the predicted salary is from the actual salary.

The key idea is:

Linear regression finds the “best fit line” by minimizing prediction errors.

Those errors are measured using Euclidean distance principles.

Why Euclidean Distance Appears

Suppose you have actual salary data:

| Experience | Actual Salary |

|---|---|

| 2 | 5 LPA |

| 4 | 8 LPA |

| 6 | 11 LPA |

The model predicts salaries using the line:Y^=b0+b1X

For each point, there is an error:Error=Y−Y^

Linear regression minimizes the total squared error:∑(Y−Y^)2

This comes directly from Euclidean geometry.

Geometric Meaning

Each data point exists in space.

For example:

- (2, 5)

- (4, 8)

- (6, 11)

The regression line tries to stay as close as possible to all points.

The “distance” from a point to the line is based on Euclidean distance.

In 2D geometry:Euclidean Distance=(x2−x1)2+(y2−y1)2

Regression simplifies this by mostly minimizing the vertical distance between actual and predicted values.

Why Squared Error Is Used

Instead of absolute distance:∣Y−Y^∣

regression uses squared distance:(Y−Y^)2

because:

- It penalizes large errors more heavily

- It is mathematically differentiable

- Optimization becomes easier using calculus

This method is called:

Ordinary Least Squares (OLS)

Your Assumption About Exponential Salary Growth

You are partially correct.

You mentioned:

salary increases exponentially

That can indeed create problems for simple linear regression.

A linear model assumes:Salary increases at a constant rate

Meaning:

- every additional year adds roughly the same salary increment.

Example:

| Experience | Salary |

|---|---|

| 1 | 4 |

| 2 | 5 |

| 3 | 6 |

This is linear.

But real-world salaries often grow non-linearly:

| Experience | Salary |

|---|---|

| 1 | 4 |

| 5 | 10 |

| 10 | 30 |

| 15 | 70 |

This is closer to exponential growth.

A straight line cannot fit such data properly.

That leads to:

- large residual errors

- inaccurate predictions

- high Euclidean distances

- poor model fit

Why the Model Gives “Erratic” Results

Because the model assumptions are violated.

Linear regression assumes:

- Linear relationship

- Constant variance

- Independent observations

- Normally distributed residuals

If salary grows exponentially:Y=b0+b1X

then residuals become large and uneven.

The optimization still minimizes Euclidean-based squared errors, but the line becomes a poor representation of the data.

Better Models for Salary Growth

Instead of linear regression, you may use:

Polynomial Regression

Y=b0+b1X+b2X2

Useful when growth curves upward.

Logarithmic / Exponential Models

If salary grows exponentially:Y=aebx

or transform data:log(Y)=b0+b1X

Tree-Based ML Models

Such as:

- Random Forest

- XGBoost

- Gradient Boosting

These capture non-linear patterns much better.

Visual Intuition

Linear regression tries to fit:

y=b0+b1x

But if real salary growth behaves more like:

y=aebx

a

b

then the straight line creates large Euclidean residual distances.

Final Summary

Euclidean calculation appears in linear regression because:

- the algorithm measures prediction error as geometric distance,

- specifically squared Euclidean distance,

- and minimizes total error using Least Squares.

Your intuition is also correct that:

- if salary growth is exponential/non-linear,

- simple linear regression performs poorly,

- causing large residual errors and unstable predictions.

In such cases, non-linear models work better.